Oil Conundrum: Record Inventory Draws And Stable Crude Prices

Something strange is taking place in oil. Crude prices have been remarkably stable over the last week, with Brent mostly trading in the high 90s on mixed prospects for the resolution of the over 7-week conflict in the Persian Gulf, despite signs to the contrary: the second round of talks between the US and Iran has been postponed indefinitely following Iran’s decision not to participate; President Trump extended a ceasefire “until such time as their proposal is submitted, and discussions are concluded, one way or the other” and the US maintains its blockade of ships departing from or heading to Iranian ports.

So while the market is rejoicing and trading at daily record highs that all is well, the oil picture remains just as bad as it was when the war started almost two months ago.

According to Goldman, the combination of 1) a lower risk premium, 2) destocking in anticipation of expected Hormuz reopening, and 3) a moderation in spot buying, helps explain why futures crude prices, physical crude prices, and refined products prices have all moderated since the ceasefire despite still low Hormuz flows and extreme draws in global visible stocks.

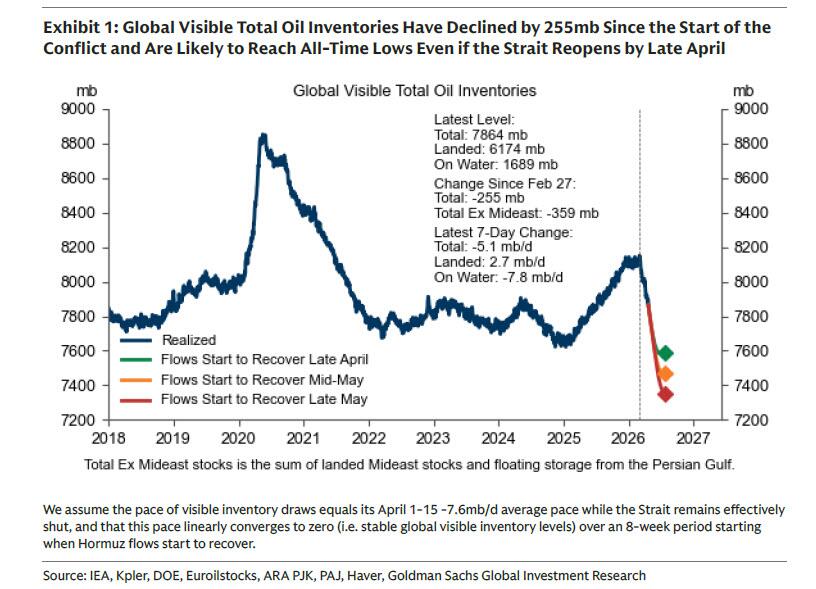

And yet, global visible oil inventories are likely to reach record-low levels even in an optimistic scenario where Hormuz flows start to recover by the end of April.

Global visible oil inventories have been drawing at an average pace of 6.3mb/d in April so far, while Goldman’s estimates of total global oil draws (including “invisible” refined products storage in non-OECD) show 10.9mb/d draws in April so far, the steepest monthly draws on record since 2017. This puts total estimated oil draws since the start of the war at 474mb.

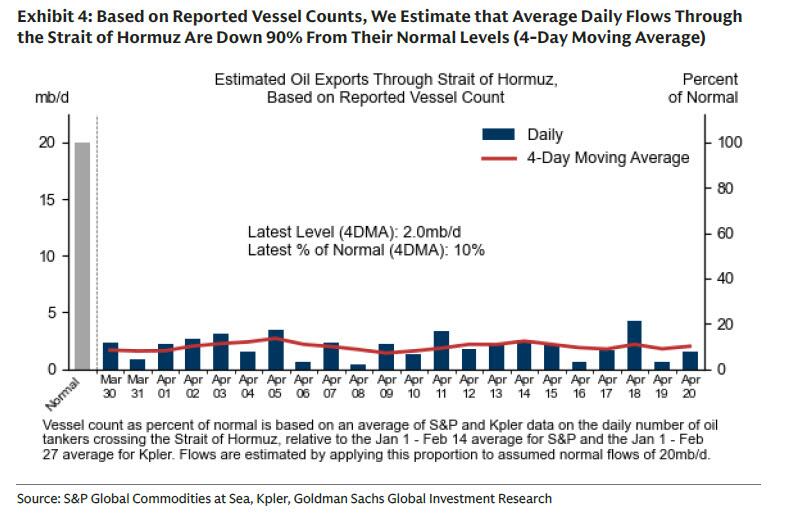

As estimated oil flows through the Strait of Hormuz remain at 10% of normal or 2.0mb/d (4-day moving average) and as any recovery in flows will likely be gradual even following a complete reopening (given logistical constraints such as reversing shut ins, tanker voyage times and pipeline speed limits), declines in global oil inventories are likely to continue through May or beyond.

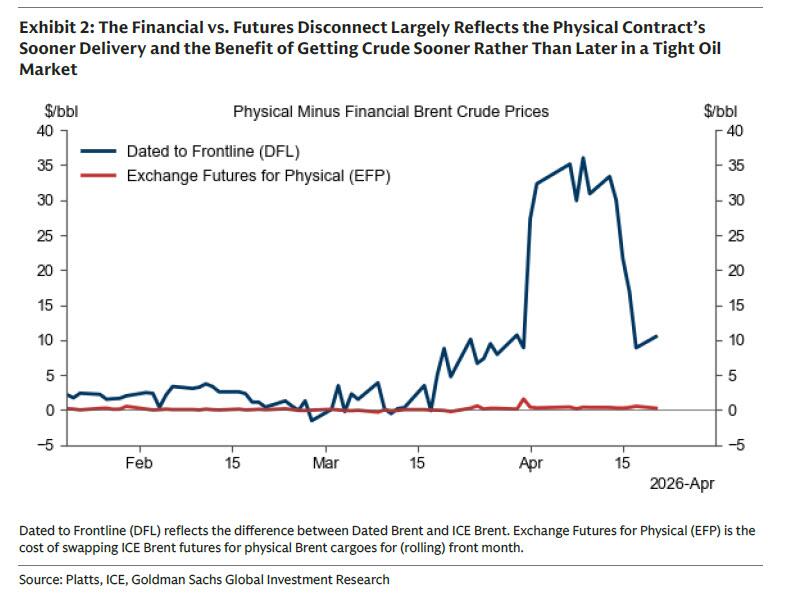

Extreme inventory draws also imply that rapidly tightening physical markets will continue to require much higher prices for immediate oil delivery rather than prices for delivery in a few months if market participants assume a high probability of a short-lived disruption. This backwardation is the key explanation of the perceived disconnect between nearby physical oil prices (i.e. prices for immediate delivery) and nearby futures oil pries (i.e. prices for June delivery).

The price of swapping Brent futures from “paper” to physical barrel delivery for the same delivery window (Exchange Futures for Physical, or EFP) never went above $2/bbl over the last two months. However, the premium for dated Brent for an immediate delivery vs.nearby futures (Dated to Frontline, or DFL) moderated recently from nearly $40/bbl to a still very high $10 as the lag between the delivery periods for both contracts narrowed.

The shift from restocking and panic buying in March to destocking in April likely explains the moderation of prices in physical markets, according to Goldman, with some Asia refineries – especially in China – reportedly re-offering previously purchased crude.

But destocking isn’t sustainable since stocks – as we explained in “How Long Before The World Hits Crude Oil Operational Minimum” – have a natural lower bound, after which the main rebalancing mechanism in the absence of a supply recovery is demand reduction.

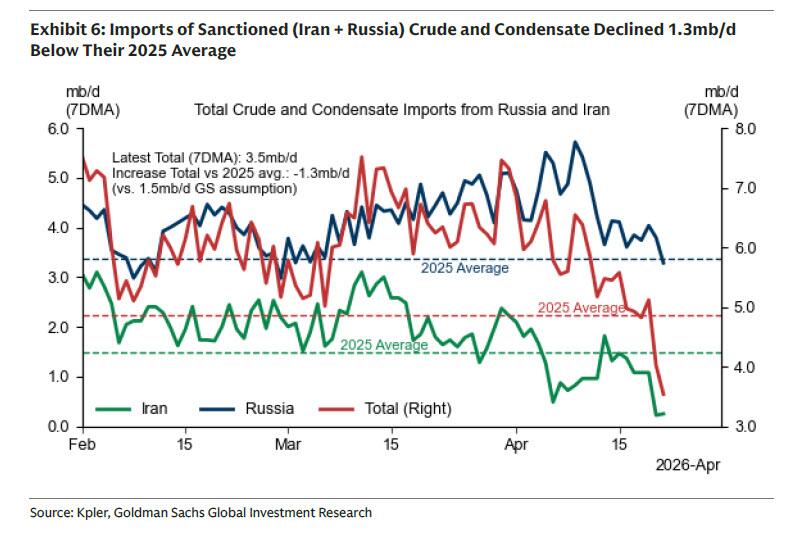

And herein lies the problem: the global oil-on-water buffer is approaching its depletion as non-sanctioned oil on water is close to its all-time lows, imports of Russian oil dipped below their 2025 average, and the US waiver on imports of Iranian oil on water expired without an extension.

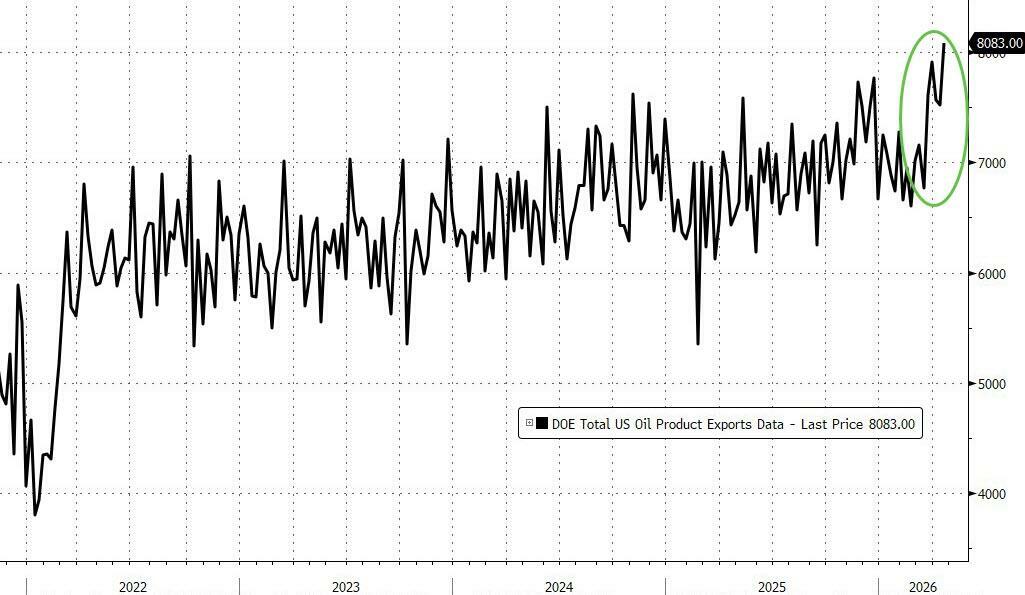

Meanwhile, US oil exports surged to a record high 12.7mb/d, as outbound shipments suggest even higher exports in May. But some key Texas pipelines are already running at or above their operational capacity, suggesting that further increases in US exports are limited.

Putting all this together, Goldman warns that while the risks to its base case oil price forecast (which is close to current market pricing) are two-sided, there is significant net upside risks from longer Hormuz flows disruptions and potentially more persistent Mideast supply losses.

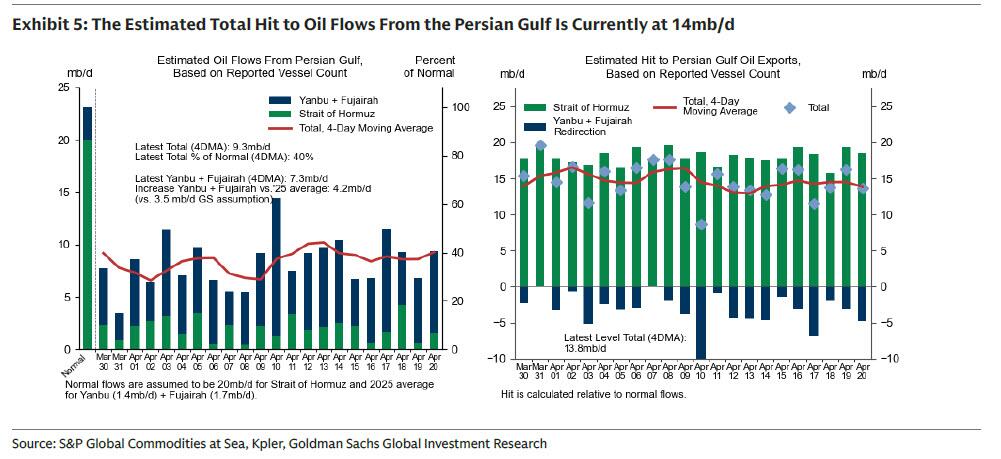

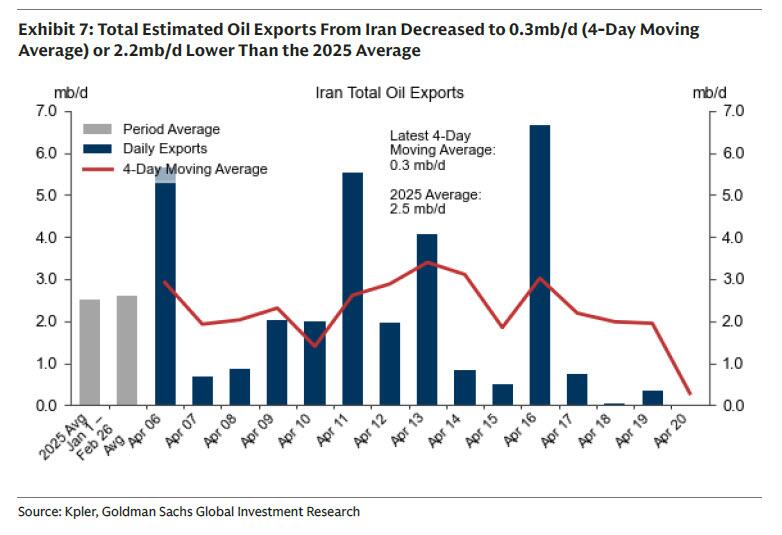

Meanwhile, as we reported previously, estimated oil flows from the Persian Gulf (including pipeline redirections) are at 9.3mb/d or 40% of normal…

… deteriorating by 2.6 mb/d which is the estimated oil exports from Iran since the US blockade started on April 12th to 0.3mb/d.

More in the full Goldman note available to pro subs.

Tyler Durden

Thu, 04/23/2026 – 00:05